Navigating Uncertainty: Energy Security and Resilience in an Evolving Regional Context

Key Insights from the RWN Executive Briefing: 12 May 2026

The RWN Executive Briefing, hosted by the Resilience World Nexus (RWN) Summit and WPC Energy, with the support of Petroleum Economist, brought together senior practitioners to provide cross-sector perspectives on energy security, operational resilience, and market risk.

The energy sector is facing a time of great uncertainty, shaped by the convergence of geopolitical conflict, volatile commodity markets, the accelerating pressures of the energy transition, and the growing physical threat of climate change to the very infrastructure the global energy system depends on. While we have to accept the complexity of the situation, we must also understand that this is a real opportunity for innovation, collaboration, and long-term resilience strategies. Leaders need to take responsibility and harness the ‘closing window of opportunity’ now more than ever, before the opportunities narrow further.

The Current Landscape

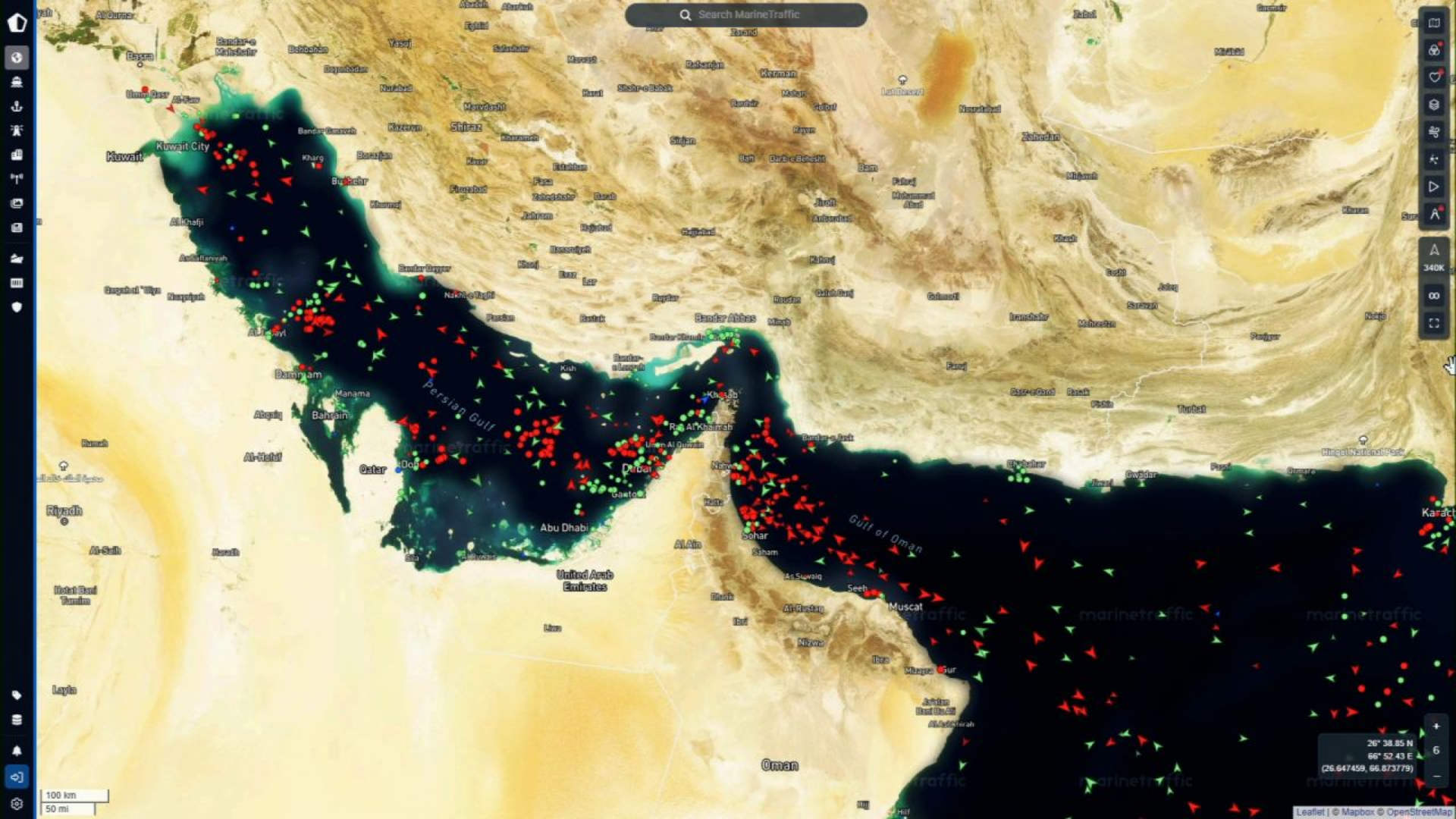

The ongoing conflict in the Middle East has sent shockwaves through global energy markets, with traffic through the Strait of Hormuz falling sharply as regional tensions have forced shipping companies to reroute and extend transit times. Far from a regional issue, this reflects a global systemic shock – a reminder that a single chokepoint can disrupt an entire global economy, and that the most destabilising variable to world trade is not reduced supply but the loss of predictability. The effects will persist for months if not years, making the shift from reactive to proactive resilience not a choice but a necessity. Meanwhile, while financial markets have bounced to near all-time highs on the back of the AI boom, rising energy costs, raw material prices, and logistics pressures are feeding through to corporate cost bases and consumers – and the market's apparent confidence is masking a far more troubling picture underneath.

Rebuilding the Global Supply Chain

Conflicts like the one in the Middle East will continue to ripple through global supply chains until organisations address a critical visibility gap. As highlighted by Ms. Catherine Cyphus, approximately 80% of supply chain disruption risk resides within Tier 2 and Tier 3 suppliers, despite fewer than 10% of organisations maintaining meaningful visibility into those tiers. The structural response to this vulnerability is already underway, accelerated by the convergence of forces that were already reshaping supply chains before the current crisis arrived – the Covid-19 pandemic, Ukraine, and the energy transition. The defining shift is regionalisation: shorter supply chains, friend-shored inputs, and a fundamental reorientation from efficiency to resilience. But the full costs of this shift – duplicated operations, increased compliance burdens, and concentration risk in the event of a regional disaster – have not yet fully materialised, and the pace of change remains uneven, with many organisations still waiting for larger players to move first. Some degree of globalisation will ultimately be preserved, precisely because global networks provide a resilience of their own.

The Three Converging Crises

The International Energy Agency has warned that the world may be entering the biggest energy crisis in history. However, the situation is more complex than a single crisis. What we are seeing is the combination of three major problems happening at the same time: geopolitical conflicts, weaknesses in countries that heavily depend on imported energy, and growing climate risks affecting energy infrastructure.

For many landlocked and import-dependent countries that are already struggling from previous shocks, energy insecurity is not a temporary problem but an ongoing challenge. At the same time, climate change is making energy systems more vulnerable. Extreme weather events such as cyclones, floods, heatwaves, and wildfires are damaging power plants, fuel facilities, and energy networks, causing further disruptions.

The most vulnerable countries sit at the intersection of all three crises. More broadly, the energy crisis is linked to some of the biggest challenges of the 2020s – the interaction between human actions, advancing technology, and climate hazards. Among these, climate disruption is likely to become the most serious long-term challenge of this century.

Building the Three Pillars of Energy Security

Energy security is a top priority for both governments and companies. While affordability and sustainability matter, reliable access to energy is still the most important factor. Energy security depends on three main areas:

-

Geographic diversification: Countries need to rely on a wider range of suppliers, not just traditional regions like the Middle East, but also places such as the Atlantic Basin, Venezuela, and Guyana.

-

Energy mix diversification: Countries need multiple energy sources. Some may continue using fossil fuels in the short term to support growth and affordability, even alongside the global shift to cleaner energy.

-

Infrastructure and access: Energy systems must be expanded and protected, especially as climate risks increasingly threaten critical infrastructure.

What Needs to Change

A global downturn is likely to affect food security, healthcare, and energy security the most, especially in vulnerable emerging economies. Avoiding these impacts requires action in three areas at the same time, although this is difficult to achieve in practice.

-

First, governments and countries should stop only reacting to crises and instead prepare for them in advance. This means setting up financial support systems that are already planned and automatically activated when risks reach a certain level, like those used in humanitarian aid.

-

Second, countries need better tools to manage risk, such as parametric insurance and risk pooling. These provide quick financial help when energy prices suddenly rise, helping to reduce wider social and economic damage.

-

Third, better coordination is needed. The information and risk data already exist, but they are spread across different organisations. The challenge is to connect data, financial tools, and policy decisions so they work together effectively.

Who Needs to Act

Addressing the energy crisis requires integrated action across the energy value chain – across government, international bodies, and the private sector.

-

Governments should create stable, long-term policies and incentives that encourage investment in all types of energy infrastructure. Consistent policy is more important than strict regulation alone.

-

International bodies need to improve coordination across regions and help align energy systems, especially where cross-border infrastructure is required.

-

Companies should be involved early in designing policies and continue investing in new energy solutions like renewables and decentralised energy systems.

Breaking down silos, motivating dialogue, and building bridges between them is not an aspiration – it is the only way to create a secure, sustainable, and inclusive energy future.

Conclusion

In many ways, the current disruption has acted as a catalyst for the energy transition, with the entire energy industry, from oil and gas, to nuclear, to renewables, trying to respond to this crisis at a real pace. For governments, energy security has risen to the top of the agenda. We are even seeing this play out among domestic households, through surging demand for solar panels and home batteries – driven not by net zero commitments, but by a simple desire for access to power at affordable rates.

Yet from another angle, we have seen such momentum in previous years, and it was lost when governments became distracted with other priorities and net zero began to fracture as a political consensus. The current uncertainty in the energy industry is just another wake-up call for the need for long-term planning. The uncomfortable truth is that we cannot keep being surprised every couple of years.

There is opportunity in systemic crisis. The question is whether this time, that opportunity will be seized – for the sake of innovation, reinvention, and the kind of structural revolution the global energy system so badly needs.

Key Takeaways

-

The most destabilizing variable to world trade is uncertainty, but this time of uncertainty is also a time of opportunity.

-

Resilience needs to be proactive – leadership today requires anticipating change, taking responsibility, and acting before crisis escalates.

-

The energy crisis is not one crisis but three converging simultaneously – geopolitical disruption, structural fragility in the most vulnerable economies, and accelerating physical risk to energy infrastructure itself – and the countries least equipped to respond sit at the intersection of all three.

-

The key priority right now is energy security, which is built on geographical diversification, energy mix diversification, and access to/ new energy infrastructures.

-

We know where the damage will land, and we have the tools to act – the problem is that the knowledge, the instruments, and the decision-makers remain in three separate silos.

-

Resilience requires integrated action across three levels – government, international bodies, and companies.

-

This crisis can be a catalyst – but only if this time, unlike the last, momentum is not lost.

These are precisely the kinds of challenges that the Resilience World Nexus Summit was built to address. In a world where energy security has become the defining strategic priority – and where geopolitical disruption, structural fragility, and climate risk are converging faster than most organisations can respond – the need for collective, cross-sector thinking has never been greater. The summit convenes C-suite executives and senior leaders who recognise that resilience is not a cost to be minimised but a strategic asset to be built. It is a forum where global decision-makers come together to turn uncertainty into advantage, and to ensure that when the next crisis arrives, and it will, they are ready. Join us in London (Church House Westminster) on the 6–7 of October.

Highlights from the Q&A

How do we educate decision-makers to make better, more informed decisions about supply chain resilience – particularly in sectors as complex as the power grid, where the criticality of issues is often hidden by a lack of understanding?

This is an age-old challenge when it comes to resilience in general, and one that is not easily fixed. However, the current crisis presents a genuine opportunity to bring resilience to the top of the agenda. Three approaches are worth considering:

-

Change Their Experience: If today’s crises are not enough for decision makers to act, it may be helpful to arrange a cross-sector simulation or scenario walk-through to role-play how decision makers would react in a high-impact crisis event. This helps decision-makers understand the significance and importance of supply chain resilience investment at a personal level.

-

Provide Evidence: Data supports investment decisions. Working with a supply-chain mapping and risk insights tool like Sentrisk to identify and quantify specific, critical risks in the supply chain, allows decision-makers to feel more confident investing in supply chain resilience strategies as it provides specifics – specific risks, specific disruption scenarios, specific outcomes.

-

Outline Scenarios: A carrot-and-stick approach can be effective. Highlighting international good practice can help decision-makers understand the scale and nature of the challenge and can also ignite a sense of competitive urgency. Aside from incentivising, there will be push factors driving change such as changing demand patterns and new regulation. Highlighting and even modelling these changes and different investment scenarios could help.

How do you see supply chains developing in the future – will they become more local or remain global, shorter or longer, and will we see increased storage at all levels?

The limits of globalisation have likely been reached, and in the short term a period of deglobalisation is expected. This means regionalisation will occur by way of shortening supply chains and reducing the size of the average footprint in order to reduce disruption risk. However, full regionalisation across all industries is neither realistic nor desirable. Globalisation brought about specialised and affordable markets which will not be easily unwound. Regionalisation brings about other risks such as concentration risk and duplicated operating and compliance costs. This means that, longer term, we will likely reach a form of hybrid set up where organisations regionalise operations which are demand-led and volatile (e.g. FMCGs), and those which are highly critical (e.g. energy infrastructure). At the same time, global connections will be maintained to preserve supply chain diversification and continued access to the affordable resources that global markets provide. Resilience, in this model, comes not from choosing between global and regional but from knowing which parts of the supply chain require which approach.

Could nuclear power, deployed at massive scale, be the solution to the energy situation in GCC countries?

Nuclear power could become an important part of the solution for GCC countries, particularly as electricity demand continues to grow, and decarbonization targets become more ambitious. That said, nuclear is not “the” single solution, but one element within a broader energy transition strategy. GCC countries have several structural advantages for a diversified low-carbon system: abundant solar resources, strong financial capacity, and growing ambitions around hydrogen and industrial decarbonization. Nuclear power can play a valuable role because it provides stable baseload power, supports grid reliability, and can help free hydrocarbons currently used for domestic power generation for higher-value export uses. The UAE’s Barakah plant is already an important reference point in the region. However, large-scale nuclear deployment also comes with challenges: very high upfront capital costs, long development timelines, water and cooling considerations, regulatory and safety requirements, as well as the need to develop specialized talent and supply chains. In practice, the most likely pathway for GCC countries may be a balanced mix of large-scale renewables (especially solar), flexible gas generation, energy storage and grid modernization, energy efficiency measures, and selective nuclear deployment where economically and strategically justified. The optimal mix will differ by country depending on demand growth, industrial strategy, export ambitions, and national policy priorities.

In a period marked by supply chain volatility, geopolitical shifts, and rapid energy transition, what strategies should PPP investors adopt to safeguard energy security and ensure resilience across Saudi and GCC infrastructure portfolios?

This is indeed one of the defining challenges for infrastructure investors in the current environment as they need to move toward a broader “resilience and strategic security” approach. Several priorities are becoming increasingly important:

- Diversification of Supply Chains: Recent disruptions have demonstrated the risks of overdependence on single geographies or suppliers. Investors should prioritize diversified procurement strategies, regional manufacturing ecosystems, and stronger local supply capabilities aligned with localization agendas such as Saudi Vision 2030.

- Long-term Contractual Resilience: PPP structures need to evolve to better allocate risks linked to inflation, commodity prices, FX volatility, and supply chain disruptions. Flexible contract mechanisms, indexed pricing structures, and robust force majeure frameworks are becoming increasingly important.

- Digitalization and Operational Resilience: Investors should place greater emphasis on smart infrastructure, predictive maintenance, cybersecurity, and real-time monitoring capabilities. Operational resilience is now as critical as physical resilience.

- Localization and Ecosystem Development: Saudi Arabia and several GCC countries are actively promoting local content and industrial development. PPP investors who build local partnerships, develop talent, and support domestic supply ecosystems will likely gain both strategic and commercial advantages over the long term.

- Climate Resilience and Transition Readiness: Infrastructure assets must increasingly be designed for extreme weather conditions, water stress, and evolving decarbonization policies. Investors should evaluate resilience not only against current risks, but also against future transition scenarios.

Overall, the GCC remains one of the world’s most attractive infrastructure investment regions due to strong demand fundamentals, ambitious national programs, and government support. However, success will increasingly depend on the ability to combine financial discipline with adaptability, localization, and long-term resilience planning.

Are there any examples you would recommend regarding procurement strategies for crude oil and supplies in the event of a closure of the Strait of Hormuz?

There are several, depending on where an organisation sits on the efficiency-to-resilience spectrum. At one end you have low cost and low flexibility strategies and at the other you have higher costs but greater levels of flexibility in thesupply chain. The strategies in between typically fall into three categories: how you work with your suppliers, supply sourcing strategies, and demand shaping.

-

How you work with your suppliers: this is about contracts and collaboration.

There are certain levers you can pull when it comes to contracts such as flexibility clauses and price averaging, but when something goes wrong, it all comes down to the relationships you have with your suppliers. By having collaborative working relationships with your suppliers, you are more likely to have early visibility of issues and have the option of working together to navigate the problem in a mutually beneficial way. Some companies go as far as to secure upstream and downstream partnerships through vertical integration.

-

Supply sourcing: this is about diversification and stockpiling.

In summary, diversification means securing multiple suppliers (ideally across different regions) to reduce supply dependencies. Increasing inventory or stockpiling means holding additional critical stock to provide a buffer in the case of disruption (this might extend to transportation capacity as well). This strategy is most applicable for critical inputs and materials such as feedstocks and highly specialised equipment with long-lead times like catalysts and production equipment.

Until now, organisations have typically seen these strategies as a cost to the business but now they are coming back into favour because they offer a very easy way to improve resilience and protect the bottom line, longer-term. Some organisations find that establishing early warning signals and monitoring helps avoid investing too much capital in stock holdings but gives them a competitive edge is supply is strained.

-

Demand shaping: this is all about intra-business collaboration to mitigate dependencies through product redesign and demand consolidation internally.

While less immediately applicable in some industries, the principle is worth considering. With demand shaping, the focus is changing the business’ demand for high-risk resources. For example, if critical energy supplies are low, can Operations, R&D, Finance and Logistics collaborate to consolidate demand. Or, if there is known geopolitical tension around a critical component, how can the organisation remove the dependency from the business through product redesign and substituting materials over time. This one is far trickier to achieve but absolutely defines resilience in the way it brings about adaptability.

Overall, the theme here is transparency and flexibility, but there is a subliminal message here too – these procurement strategies require the business to work together in what is called an ‘Enterprise-wide Approach’.

This article was authored by the Resilience World Nexus Summit (RWN) team.

www.rwnsummit.com

Gain further insights from industry leaders on the evolving energy landscape, key transition challenges, and the opportunities shaping the future of the sector.